Happy Monday and welcome back to the land of blinking screens. I don’t know about you, but I’ve been intrigued lately by all the projections/prognostications that analysts feel compelled to provide at the beginning of each year. So, just for fun, I thought I’d join in the game this year.

To be clear, I do NOT manage money based on predictions, macro views, or the proverbial gut hunches. No, I prefer to stick to the weight of the evidence from a plethora of market models. I strive to keep portfolios positioned in line with what “is” happening in the market and not what I think “should” to be happening in the market. I learned a LONG time ago that Ms. Market doesn’t give a hoot about what I think “ought” to be happening in her game and that my primary job is to try and get it mostly right, most of the time.

However, I’m also known in the business as a bit of a model geek. So, I decided to try my hand at “modeling” the outlook for the S&P 500 this year. But as I hope I’ve made clear, this is a “just for fun” exercise.

The Market Drivers

I decided to start with what I believe to be the primary drivers of stock market returns. Namely the economy, earnings, monetary conditions, inflation, the technical health of the market, and historical market cycles.

I then dug into my trusty model toolbox and dug out indicators and/or models for each of these components. Or in some cases, I combined multiple models to create a composite model.

The Models

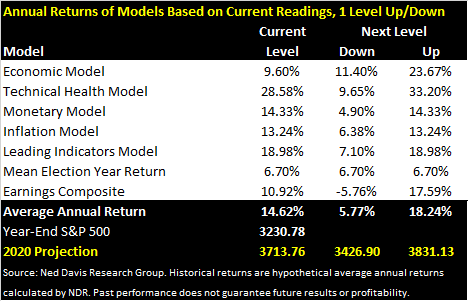

I wound up with seven models. Next, I looked at the average annual historical return of the S&P 500 for the current reading/mode of each model. I have to give a hat tip to the computers at Ned Davis Research Group for this data. I then averaged the historical returns and applied it to the S&P’s year end closing price of 3230.78. This gave me a projection for year.

As the first column in the chart below details, the average historical return given the “Current Level” of the models has been +14.62%. This produces a 2020 projection of 3714. Not too shabby, right?

Playing What If

But, but, but… The flaw in the ointment here is that things change in the market game – sometimes quickly and monumentally. The most obvious example of a model that can change dramatically in a relatively short period of time would be the Technical Health Model, which measures the technical state of 157 sub-industry groups on a weekly basis. In other words, this is a price-based model that is likely to change throughout the next 12 months.

With this in mind, I decided to look at the historical returns of the models if they ALL moved DOWN one notch in their readings/modes.

Not surprisingly, the average historical return drops from +14.6% to +5.77%. This is actually more in line with the throngs of Wall Street analysts who are calling for “low, single-digit returns” this year. Interesting.

Next, since I’m a card-carrying member of the-glass-is-half-full club, I decided to also look at the average historical returns for the models if the reading/modes moved UP one notch from current levels. Given that several of the models are already in their most upbeat modes, the average annual historical return wasn’t too dramatic – the average increased only to +18.24%. But again, I’d certainly take a high teens gain in 2020!

Summing Up

Finally, I decided that saying the market should rise between 5.8% and 18.2% was a bit of a cop out as that’s a pretty big range!

What I’m going to do then is take the average of the “Next Level Up/Down” returns as my “final answer.” So, drum-roll please… My “just for fun,” model-based guesstimate for the S&P 500 in 2020 is 12.0%. This would put the close next New Year’s Eve at 3618.47. That’s my story and I’m sticking to it. Unless of course, things change – then I’ll simply do what I always do and adapt to conditions – ha!

Since it’s the start of a new week, it’s now time to put aside my subjective view of the action and to review the “state” of our indicator boards. Each week we do a disciplined, deep dive into our key market indicators and models. The overall goal of this exercise is to (a) remove emotion from the investment process, (b) stay “in tune” with the primary market cycles, and (c) remain cognizant of the risk/reward environment.

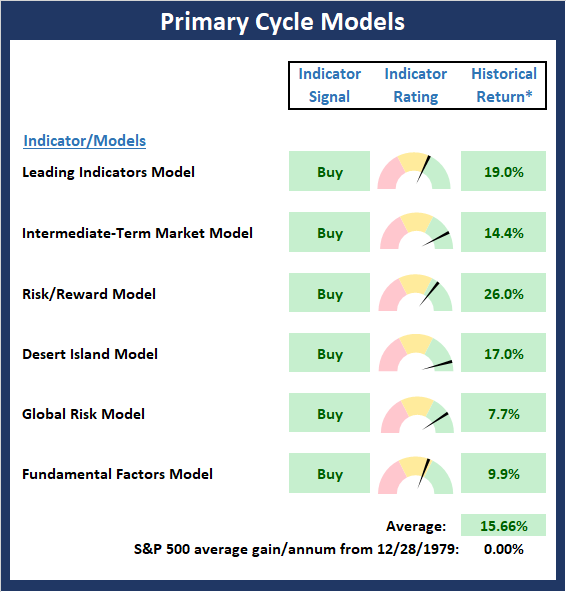

The Major Market Models

We start with six of our favorite long-term market models. These models are designed to help determine the “state” of the overall market.

The are no changes whatsoever to the Primary Cycle board this week. So, as I’ve been saying for many moons now, the status of my favorite big-picture market models continues to suggest that the bulls are in charge of the game and that investors should keep their offense on the field.

This week’s mean percentage score of my 6 favorite market models held rose to 74.3% from 71.8% while the median upticked to 75.0% from 72.5%.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability – NOT INDIVIDUAL INVESTMENT ADVICE.

View My Favorite Market Models Online

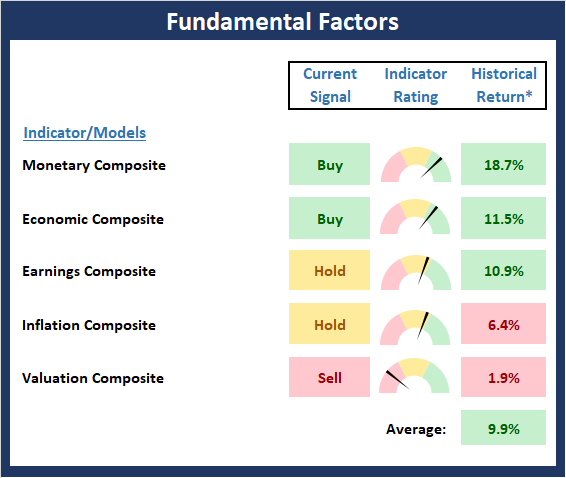

The State of the Fundamental Backdrop

Next, we review the market’s fundamental factors in the areas of interest rates, the economy, inflation, and valuations.

Ditto for the Fundamental Factors board, as the status of the board held steady this week. From my seat, this board tells me to look at 2020 from an upbeat perspective. What would change my view, you ask? If either the economic or earnings composite were to move into negative territory, or if the Fed would need to shift their stance, then I would likely consider moving to a less offensive stance.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability – NOT INDIVIDUAL INVESTMENT ADVICE.

View Fundamental Indicator Board Online

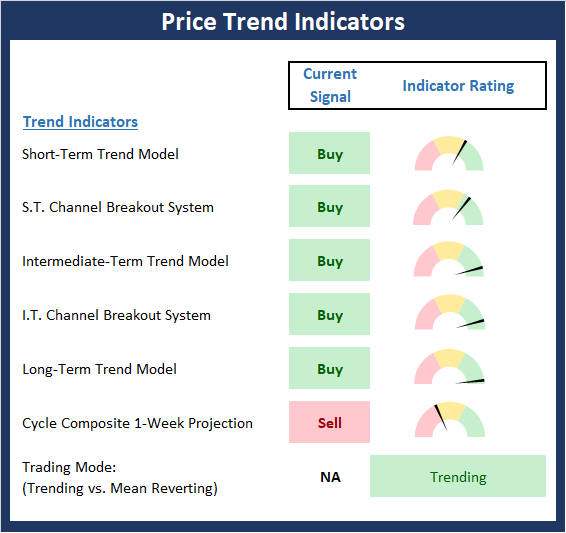

The State of the Trend

After looking at the big-picture models and the fundamental backdrop, I like to look at the state of the trend. This board of indicators is designed to tell us about the overall technical health of the current trend.

Frankly, I’m a little surprised that the Trend board remains in such good shape. I’m likely not the only investor who has been expecting the bears to make a stand at some point here. But despite the drama in Washington and what looked for a minute like a hot war in Iran, any/all dips continue to be bought. And until this trend changes, one must give the bulls the benefit of any/all doubt.

NOT INDIVIDUAL INVESTMENT ADVICE.

View Trend Indicator Board Online

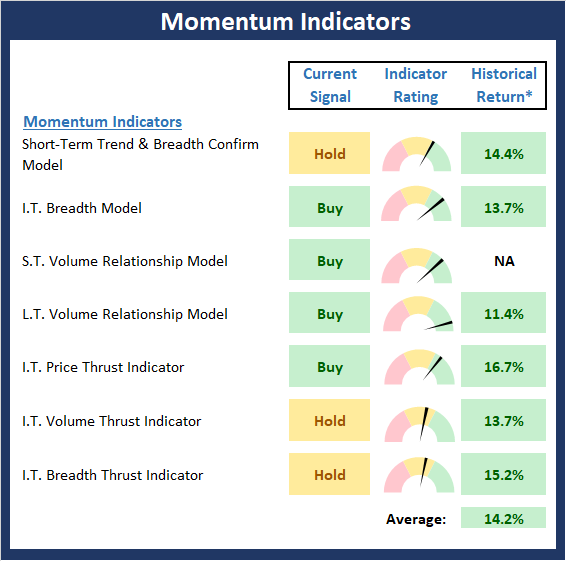

The State of Internal Momentum

Next, we analyze the “oomph” behind the current trend via our group of market momentum indicators/models.

Despite a little slippage in the indicators last week, the Momentum board remains in pretty good shape. To be clear, the board is not in pound-the-table bullish shape. However, it is certainly “good enough” to keep the bulls in business.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability – NOT INDIVIDUAL INVESTMENT ADVICE.

View Momentum Indicator Board Online

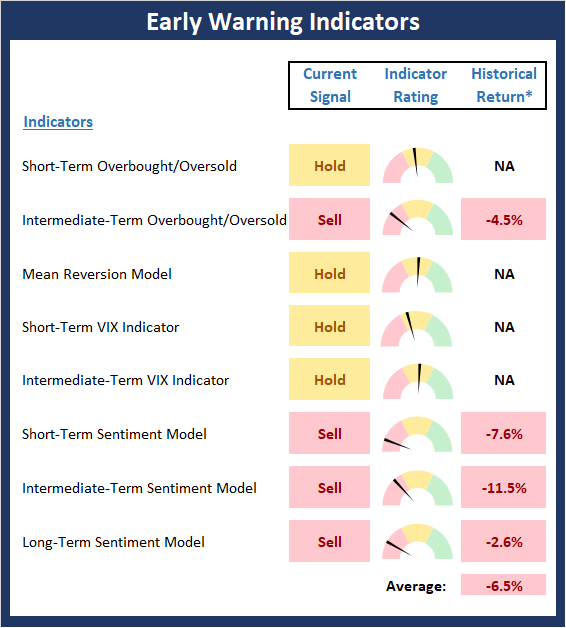

Early Warning Signals

Once we have identified the current environment, the state of the trend, and the degree of momentum behind the move, we then review the potential for a counter-trend move to begin. This batch of indicators is designed to suggest when the table is set for the trend to “go the other way.”

The Early Warning board continues to act like a 3rd grader in the back of the class desperately waving his hand because he/she knows the answer to the question the teacher has asked. The bottom line is the market remains overbought and sentiment is overly positive. Thus, the table is indeed set for our furry friends in the bear camp. But as I wrote last week, the big question is if the bear camp will be able to do anything with their opportunity. Finally, it is important to remember that when a market gets overbought and stays overbought, it is a positive. In other words, this is known as a “good overbought” condition and a sign of strength. However, I’m probably not the only one feeling a little deja vu here (January 2018) and wondering what is going to come out of the woodwork next.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability – NOT INDIVIDUAL INVESTMENT ADVICE.

View Early Warning Indicator Board Online

A fool thinks himself to be wise, but a wise man knows himself to be a fool. -Shakespeare

All the best,

David D. Moenning

Investment Strategist

Disclosures

At the time of publication, Mr. Moenning and/or Redwood Wealth Management, LLC held long positions in the following securities mentioned: None

Note that positions may change at any time.

NOT INVESTMENT ADVICE. The opinions and forecasts expressed herein are those of Mr. David Moenning and Redwood Wealth and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as investment recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

Mr. Moenning and Redwood Wealth may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

The analysis provided is based on both technical and fundamental research and is provided “as is” without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

{kind=link}